Transfer pricing deals with transactions between “associated entities” and ensures that connected parties calculate taxable profits on an arm’s length basis, as if the transactions were taking place between independent businesses. Without these rules, groups could obtain unfair tax advantages by shifting profits to low-tax jurisdictions or reducing profits in higher-tax jurisdictions.

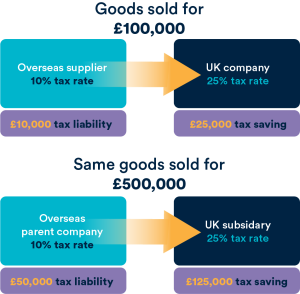

The illustration below shows a simplified example of how pricing between connected parties can affect the overall tax position of a group.

In a transaction between unconnected parties, goods are sold at market value, resulting in a balanced allocation of profit and tax. However, where the parties are connected, there may be an incentive to increase the price charged, shifting profits to a lower-tax jurisdiction and reducing the group’s overall tax liability.

Transfer pricing rules are designed to prevent this by ensuring transactions reflect true market value.

How do you calculate an arm’s length price?

There are five recognised transfer pricing methods which can be used to determine an arm’s length price:

- Comparable Uncontrolled Price (CUP)

- Resale Price Method (RPM)

- Cost Plus Method (CPM)

- Transactional Net Margin Method (TNMM)

- Profit Split Method (PSM)

The most appropriate method will depend on the nature of the transaction, and it is common for different methods to be applied across different types of transactions within the same group.

A functional analysis is typically carried out to understand the transaction in detail, including the functions performed by each party, the risks assumed, and the assets used. This is then supported by benchmarking analysis, comparing the pricing or profitability of the transaction with similar arrangements between independent businesses.

Who do transfer pricing rules apply to?

Broadly speaking, all entities should calculate taxable profits and losses on an arm’s length basis, particularly where overseas parties are involved. There is, however, an SME exemption within UK transfer pricing legislation. A company will generally qualify as an SME if it meets the following criteria:

| Small Enterprise | Medium enterprise | |

| Turnover | Less than €10m | Less than €50m |

OR

| Balance sheet asset total | Less than €10m | Less than €50m |

AND

| Employees | Less than 50 | Less than 250 |

A company must meet the employee threshold and either the turnover or balance sheet threshold.

When assessing SME status, the position of connected companies must also be considered. This includes not only wholly owned subsidiaries, but also entities where there is a shareholding of 25% or more. As a result, SME status should be reviewed regularly, particularly where group structures change. It is also important to note that the SME exemption is not absolute. It may not apply where transactions involve certain overseas jurisdictions, or where HMRC issues a transfer pricing notice. In addition, other anti-avoidance rules may still require transactions to be priced on an arm’s length basis. Finally, overseas jurisdictions may not offer the same exemptions, meaning SMEs can still be subject to transfer pricing requirements outside the UK.

What transactions do transfer pricing rules apply to?

Transfer pricing can apply to all transactions between connected parties. For accounting periods beginning on or after 1 January 2026, a UK-to-UK exemption will largely remove the requirement to apply transfer pricing rules to domestic transactions. However, there are exceptions, so reviews are still recommended.

Common examples of transactions include:

- Sale of goods

- Provision of management services (e.g. finance, HR, IT)

- Overseas sales functions

- Intercompany loans

- Royalties and intellectual property licences

Branches and permanent establishments

Transfer pricing principles also apply where an overseas entity operates through a UK branch or permanent establishment. In these cases, the “separate entity” principle is applied, meaning the branch is treated as if it were an independent entity. Transfer pricing is then used to determine how profits should be allocated to the UK.

I’m not legally required to prepare transfer pricing documentation, so why should I?

Even where there is no strict legal requirement to prepare transfer pricing documentation, there are a number of practical benefits. Putting appropriate policies and pricing mechanisms in place early provides clarity and consistency as a business grows. It avoids the need to revisit or reconstruct arrangements retrospectively, which can be both time-consuming and higher risk. It also provides greater certainty when expanding internationally, particularly where overseas tax authorities may require documentation regardless of UK exemptions.

From a commercial perspective, clear transfer pricing policies can improve internal reporting and governance by ensuring that divisional performance is not distorted by non-commercial pricing. Finally, well-documented transfer pricing can be valuable in the context of investment or a sale, helping to demonstrate that tax risks have been considered and managed appropriately.

How can Wilson Partners help?

Wilson Partners can review your group structure and transactions to assess your transfer pricing requirements under UK legislation.

We can support with the design and implementation of transfer pricing policies, advise on appropriate pricing methodologies, and prepare documentation to demonstrate that transactions have been carried out on an arm’s length basis.